All Categories

Featured

Table of Contents

The drawbacks of boundless financial are frequently forgotten or not discussed in any way (much of the information available regarding this idea is from insurance representatives, which might be a little prejudiced). Only the cash money worth is expanding at the returns rate. You likewise need to pay for the expense of insurance, charges, and expenditures.

Every permanent life insurance plan is different, however it's clear a person's total return on every buck spent on an insurance coverage product could not be anywhere close to the returns rate for the policy.

Royal Bank Infinite Visa Rewards

To give a really fundamental and hypothetical instance, let's assume a person has the ability to make 3%, typically, for every single buck they invest in an "limitless financial" insurance policy item (after all costs and costs). This is double the approximated return of whole life insurance policy from Consumer Information of 1.5%. If we think those dollars would certainly be subject to 50% in tax obligations complete if not in the insurance coverage item, the tax-adjusted rate of return can be 4.5%.

We assume greater than typical returns overall life product and a very high tax obligation price on dollars not take into the policy (that makes the insurance product look far better). The reality for many individuals may be worse. This fades in contrast to the lasting return of the S&P 500 of over 10%.

Limitless banking is a wonderful item for agents that sell insurance, yet might not be optimal when contrasted to the more affordable alternatives (without any sales individuals gaining fat payments). Right here's a break down of several of the various other supposed advantages of limitless financial and why they might not be all they're gone crazy to be.

Infinite Banking Reviews

At the end of the day you are buying an insurance coverage product. We like the defense that insurance policy provides, which can be gotten much less expensively from an inexpensive term life insurance policy policy. Overdue car loans from the plan might likewise reduce your fatality advantage, lessening another degree of defense in the plan.

The idea just works when you not only pay the significant premiums, yet use added cash money to acquire paid-up enhancements. The chance price of every one of those bucks is significant exceptionally so when you might instead be investing in a Roth IRA, HSA, or 401(k). Even when contrasted to a taxed financial investment account or also a savings account, boundless financial might not offer comparable returns (compared to spending) and similar liquidity, access, and low/no charge framework (compared to a high-yield interest-bearing accounts).

With the rise of TikTok as an information-sharing system, economic guidance and techniques have actually located a novel way of spreading. One such approach that has been making the rounds is the unlimited banking idea, or IBC for short, garnering endorsements from celebrities like rap artist Waka Flocka Flame. Nonetheless, while the technique is presently popular, its roots trace back to the 1980s when financial expert Nelson Nash introduced it to the globe.

Within these plans, the cash money worth grows based on a price set by the insurance provider. Once a significant cash money worth builds up, insurance holders can acquire a cash worth financing. These loans vary from traditional ones, with life insurance serving as security, meaning one might lose their coverage if borrowing exceedingly without ample cash money value to support the insurance coverage expenses.

Private Banking Concepts

And while the attraction of these plans appears, there are innate restrictions and risks, requiring thorough cash worth surveillance. The method's legitimacy isn't black and white. For high-net-worth people or company owners, especially those utilizing techniques like company-owned life insurance coverage (COLI), the advantages of tax breaks and substance development might be appealing.

The appeal of unlimited financial does not negate its challenges: Cost: The fundamental need, a long-term life insurance policy plan, is more expensive than its term counterparts. Qualification: Not everybody qualifies for entire life insurance coverage due to extensive underwriting processes that can exclude those with specific health or way of life conditions. Complexity and risk: The elaborate nature of IBC, coupled with its threats, may deter lots of, especially when simpler and much less risky options are available.

Allocating around 10% of your regular monthly revenue to the policy is simply not feasible for a lot of people. Part of what you review below is simply a reiteration of what has already been stated above.

Prior to you get yourself right into a circumstance you're not prepared for, understand the complying with initially: Although the principle is frequently offered as such, you're not really taking a lending from on your own. If that were the situation, you wouldn't have to repay it. Instead, you're borrowing from the insurer and have to settle it with passion

Infinite Banking Strategy

Some social media sites blog posts recommend making use of cash money worth from whole life insurance policy to pay for charge card financial debt. The idea is that when you pay back the car loan with interest, the amount will certainly be returned to your investments. Regrettably, that's not exactly how it works. When you repay the car loan, a section of that passion mosts likely to the insurance policy company.

For the very first several years, you'll be settling the compensation. This makes it very hard for your plan to accumulate value throughout this time around. Entire life insurance policy prices 5 to 15 times much more than term insurance coverage. Many people merely can't afford it. So, unless you can manage to pay a few to several hundred dollars for the following decade or even more, IBC won't help you.

If you call for life insurance coverage, right here are some beneficial tips to take into consideration: Consider term life insurance. Make certain to go shopping about for the finest rate.

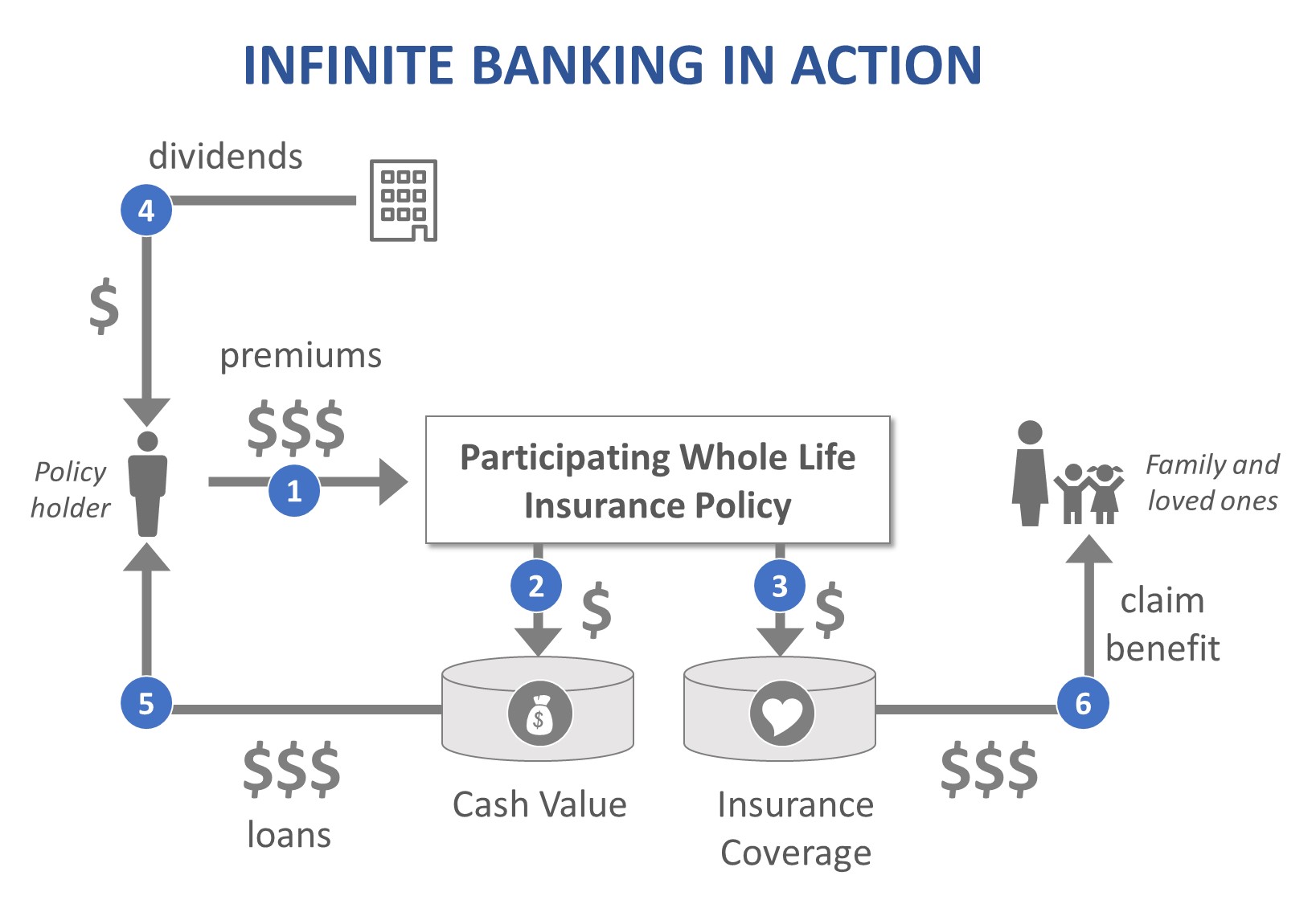

Limitless financial is not a service or product offered by a details establishment. Boundless banking is a method in which you get a life insurance plan that collects interest-earning cash worth and get car loans versus it, "obtaining from yourself" as a source of resources. Then at some point repay the finance and start the cycle around once more.

Pay plan premiums, a section of which constructs cash money value. Cash value gains worsening passion. Take a financing out versus the policy's cash value, tax-free. Settle loans with passion. Cash value accumulates again, and the cycle repeats. If you utilize this principle as planned, you're taking cash out of your life insurance policy plan to buy whatever you would certainly require for the rest of your life.

{kind=link}

Latest Posts

Create Your Own Banking System With Infinite Banking

Paradigm Life Infinite Banking

Non Direct Recognition Life Insurance Companies